Strengthening Rural Growth with Enhanced Agricultural Credit: A Pathway to Inclusive Development

(Relevant for Sociology Paper 2: Rural and Agrarian transformation in India)

|

Rural India stands at a crossroads. While agriculture remains the backbone of the rural economy, its challenges and opportunities are rapidly evolving. Recognizing this, the Union Finance Minister has urged rural banks to increase agricultural credit disbursement to meet the changing financial needs of New Rural India. This call comes amid a review of Karnataka Grameena Bank’s performance in Ballari, underscoring the critical role rural financial institutions play in catalyzing growth. The Role of Agricultural Credit in Rural IndiaAgricultural credit is vital for farmers to meet both their day-to-day needs and long-term investments. Formal sources of credit in India include public sector banks (such as State Bank of India), Regional Rural Banks (RRBs), cooperatives, and the National Bank for Agriculture and Rural Development (NABARD). Types of Agricultural Credit

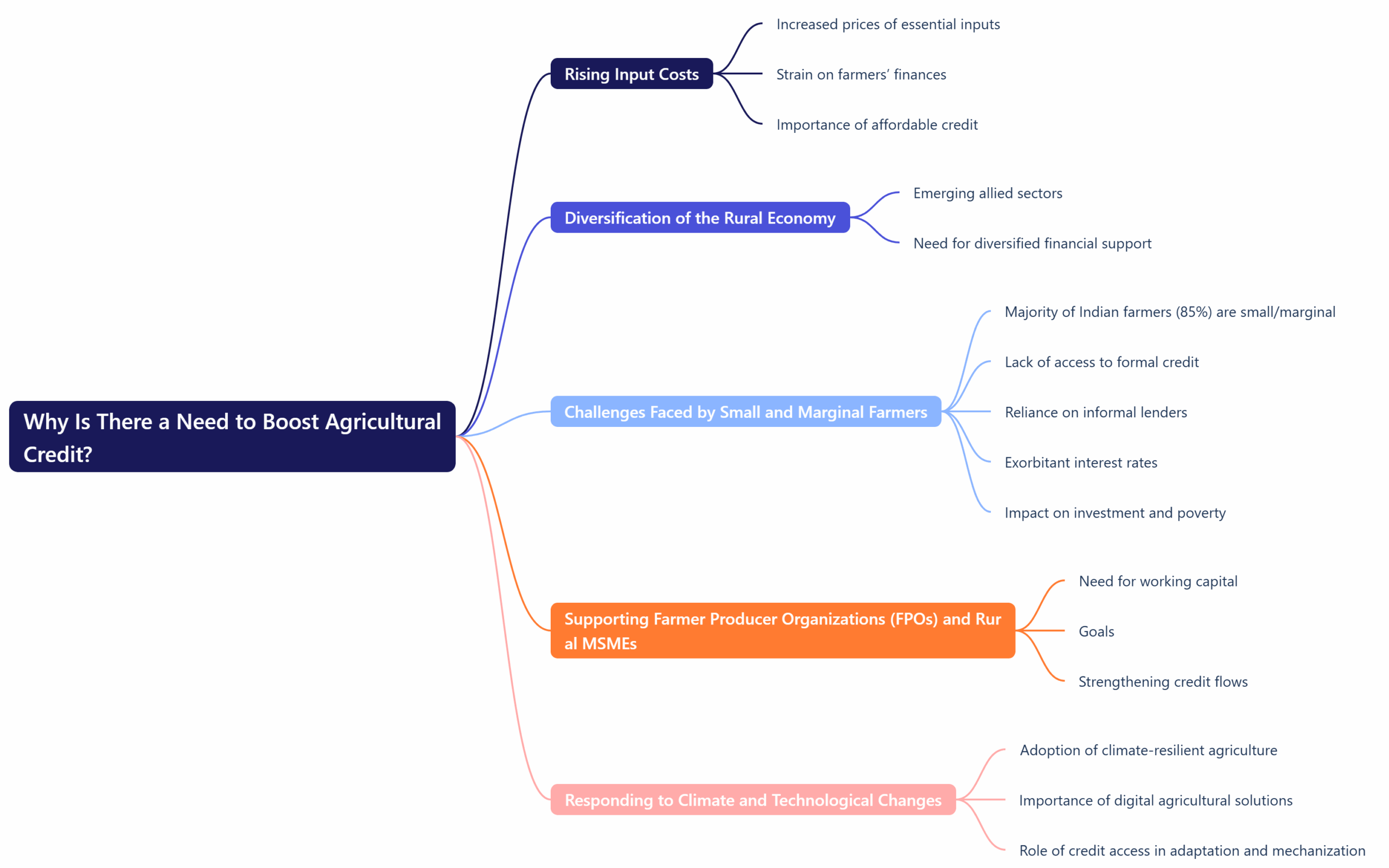

Access to timely and affordable credit is crucial to enabling farmers to invest in productivity-enhancing inputs and technology, and thereby secure their livelihoods. Why Is There a Need to Boost Agricultural Credit?

The cost of essential agricultural inputs has increased significantly in recent years. Seeds, fertilizers, machinery, and irrigation equipment have become more expensive, straining farmers’ finances. Affordable credit is essential for farmers to keep pace with these rising costs.

Modern rural India is no longer dependent solely on traditional farming. Allied sectors such as dairy, fisheries, food processing, and agri-tech startups are emerging, demanding diversified financial support that traditional agricultural credit often overlooks.

Nearly 85% of Indian farmers belong to small and marginal categories. Unfortunately, many lack access to formal credit and are forced to rely on informal lenders charging exorbitant interest rates. This financial exclusion limits their ability to invest in productive assets and escape poverty traps.

FPOs and rural Micro, Small, and Medium Enterprises (MSMEs) need working capital to improve supply chains, value addition, and market access. Strengthening credit flows to these entities can enhance rural economies and foster collective growth.

Adoption of climate-resilient agriculture and digital agricultural solutions requires financial backing. Credit access is vital to enabling farmers to adapt to climate risks and embrace mechanisation and digital tools. Government Measures to Boost Agricultural Credit

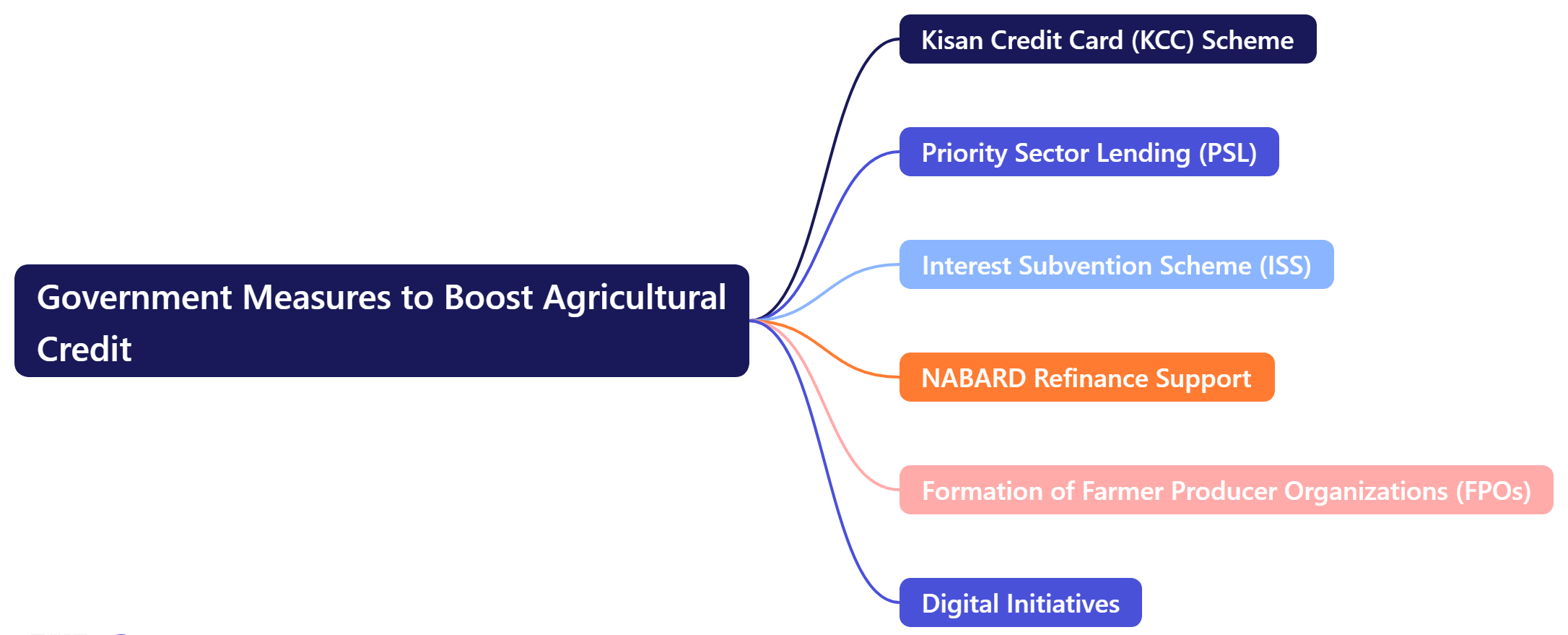

Several policies and initiatives have been introduced to enhance credit flow to the agricultural sector.

This flagship scheme provides farmers with timely and adequate credit for their agricultural needs. It simplifies access and reduces dependency on informal sources.

Banks are mandated to lend 18% of their Adjusted Net Bank Credit (ANBC) to agriculture, ensuring a minimum flow of credit to the sector.

The scheme offers concessional interest rates, particularly during calamities or delayed cropping seasons, helping farmers maintain liquidity.

NABARD extends low-cost refinance support to rural financial institutions, strengthening their ability to lend and support rural development projects.

The government targets creating 10,000 FPOs to empower farmers collectively. Supported by NABARD and the Small Farmers’ Agribusiness Consortium (SFAC), FPOs enhance farmers’ bargaining power and access to credit.

Efforts like Digital KCC, Agristack, and Jan Dhan-Aadhaar-Mobile (JAM) integration streamline loan disbursement and reduce leakages, making credit delivery more efficient. Challenges in Agricultural Credit Delivery

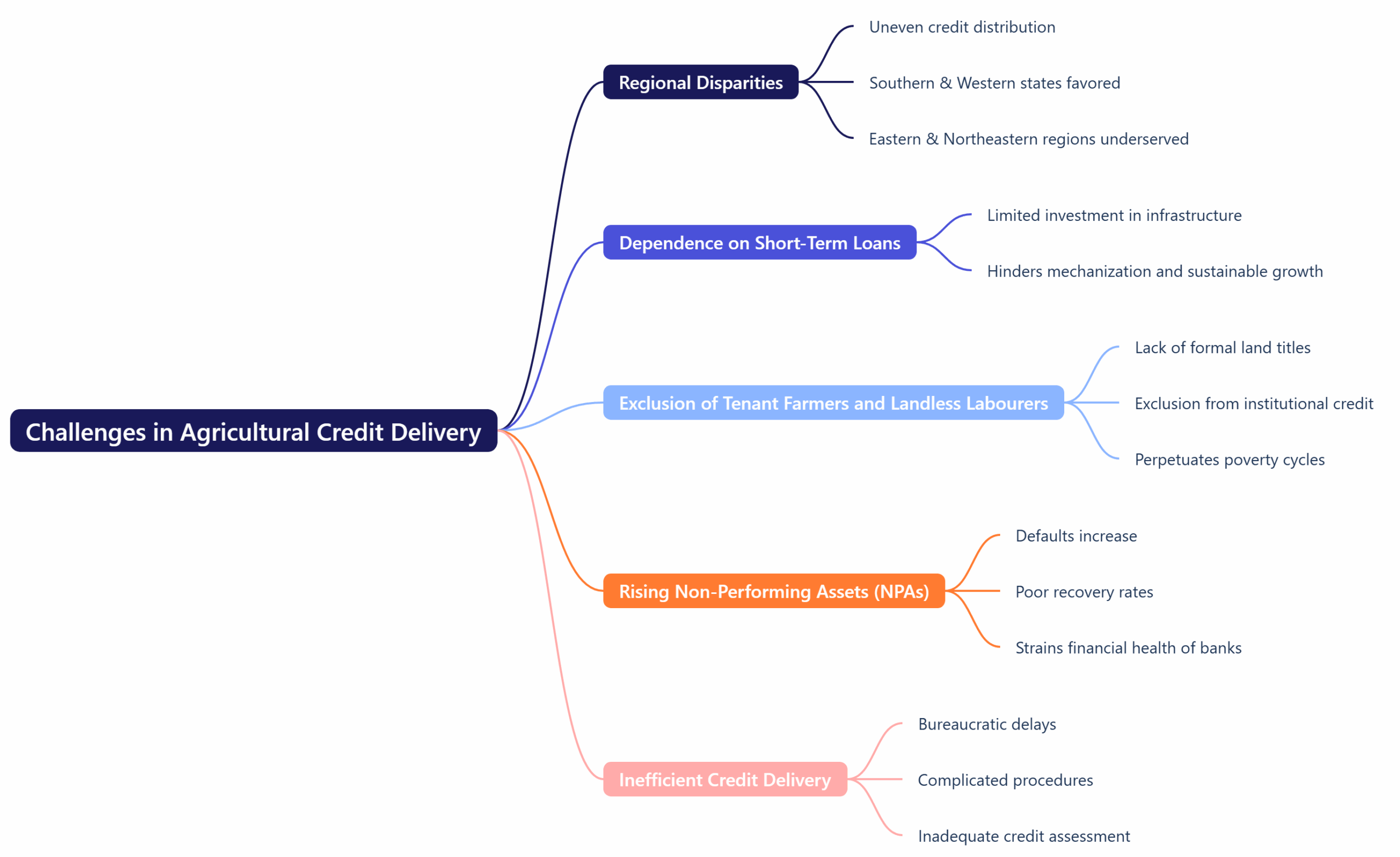

Despite these measures, several obstacles persist.

Credit distribution is uneven, with Southern and Western states receiving a disproportionate share. Eastern and Northeastern regions remain underserved, exacerbating regional inequalities.

Most agricultural credit is short-term, which limits investment in infrastructure and mechanisation necessary for sustainable growth.

Millions lack formal land titles and are thus excluded from institutional credit, perpetuating cycles of poverty and vulnerability.

Defaults and poor recovery rates strain the financial health of Regional Rural Banks and cooperative institutions, affecting their lending capacity.

Bureaucratic delays, complicated procedures, and inadequate credit assessment reduce the effectiveness of credit schemes. Sociological Insights: Understanding Rural Credit and GrowthFrom a sociological perspective, enhancing agricultural credit is not merely an economic issue but a crucial step towards social inclusion and empowerment.

Land ownership and caste hierarchies influence access to credit, often marginalizing tenant farmers and landless laborers. Expanding credit to these groups can help break structural inequalities.

The rise of FPOs reflects the power of collective agency in rural areas, aligning with sociological theories emphasizing social capital and networks as engines of development.

Credit availability enables rural communities to adopt new technologies and diversify livelihoods, driving modernization and shifting traditional social roles. The Way Forward: Policy and Practice Recommendations

Empowering RRBs and cooperative banks through capital infusion, digital infrastructure, and robust risk management frameworks will enhance their capacity to serve rural borrowers.

Broadening credit to allied rural sectors like dairy, fisheries, food processing, and renewable energy will diversify income sources and reduce agricultural dependence.

Facilitating access through Joint Liability Groups (JLGs) and Self-Help Groups (SHGs) will bring excluded groups under formal credit umbrellas, promoting gender and social equity.

AI-based credit scoring, satellite imagery, and digital record-keeping can improve loan targeting, reduce fraud, and speed up disbursement.

Coordinated efforts between the Finance Ministry, NABARD, and state governments are necessary to improve outreach and address regional disparities effectively. Conclusion: Building a Resilient Rural EconomyEnhancing agricultural credit is pivotal for strengthening rural growth and inclusive development. It empowers farmers to invest in productivity, embrace diversification, and build resilience against climate and market uncertainties. However, credit alone cannot transform rural India. It must be accompanied by social inclusion policies, improved infrastructure, and capacity building. Only through such integrated approaches can we realize the vision of a prosperous and equitable rural economy, fulfilling the promise of New Rural India. |

To Read more topics, visit: www.triumphias.com/blogs

Read more Blogs:

Echoes of Life and Loss: A Sociological Inquiry into India’s Vital Statistics 2023

Health for All, or Health for Some? Ayushman Bharat and the Promise of Universal Coverage