Introduction: Powering Progress: India’s Transition to Electric Vehicles

India’s transition to electric vehicles (EVs) is not just a technological transformation, but a critical step towards achieving sustainable development, reducing urban air pollution, cutting oil imports, and meeting its international climate commitments. As the world’s third-largest emitter of greenhouse gases and one of the fastest-growing automobile markets, India’s electric mobility shift is central to its green growth story

The Need for Electric Vehicles in India

India faces multiple challenges related to transport emissions:

Air pollution: Transport is a major contributor to urban air quality deterioration. According to a 2024 CPCB report, vehicular emissions account for 28% of particulate matter in major cities.

Oil import dependence: India imports over 85% of its crude oil, causing economic vulnerability. In FY 2023–24, India spent nearly $158 billion on oil imports.

Climate goals: Under the updated NDCs (Nationally Determined Contributions), India aims to reduce its carbon intensity by 45% by 2030 (from 2005 levels) and achieve net-zero emissions by 2070.

Electric vehicles, with zero tailpipe emissions and lower lifecycle costs, offer a clear path to addressing these concerns.

Government Policies and Initiatives

The Government of India has launched a series of policies to promote electric mobility:

Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME)

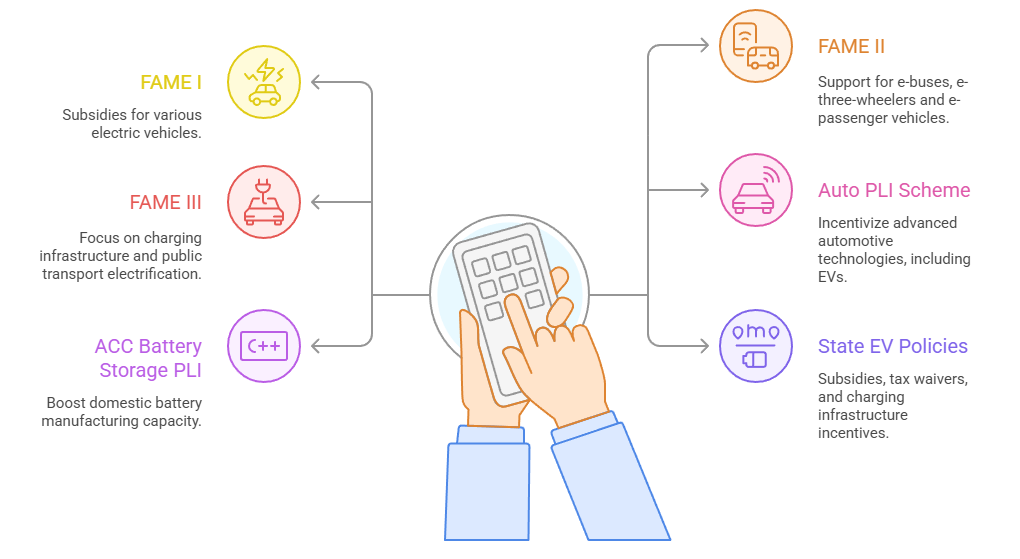

FAME I (2015-2019): Offered subsidies for electric two-wheelers, cars, and buses.

FAME II (2019-2024): Allocated ₹10,000 crore to support demand for 7,000 e-buses, 5 lakh e-three-wheelers, 55,000 e-passenger vehicles, and 10 lakh e-two-wheelers.

FAME III (expected by late 2025): Proposed to focus on expanding charging infrastructure and electrification of public transport.

Production Linked Incentive (PLI) Schemes

Auto PLI Scheme: ₹25,938 crore outlay to incentivize advanced automotive technologies, including EVs.

Advanced Chemistry Cell (ACC) Battery Storage PLI: ₹18,100 crore to boost domestic battery manufacturing capacity up to 50 GWh.

State EV Policies

Over 24 Indian states/UTs have announced dedicated EV policies. States like Delhi, Maharashtra, Tamil Nadu, and Gujarat offer attractive subsidies, road tax waivers, and incentives for setting up charging infrastructure.

Market Growth and Trends

India’s EV market is witnessing robust growth:

Sales Surge: EV sales crossed the 2.2 million mark in FY 2023–24, nearly doubling from the previous year.

Two-wheelers dominate, with over 65% market share.

Three-wheelers (e-rickshaws and autos) comprise 25%.

Electric cars and buses are rapidly gaining traction, especially in urban mobility and public transport sectors.

OEM Participation: Players like Tata Motors, Mahindra Electric, Ather Energy, Ola Electric, and TVS are expanding portfolios. Global majors like Hyundai, MG, and BYD have also entered India’s EV market.

Startups and Innovation: EV ecosystem is supported by 450+ startups focusing on battery tech, charging, and mobility platforms.

Charging Infrastructure: Backbone of EV Adoption

Charging remains a critical bottleneck. To address this:

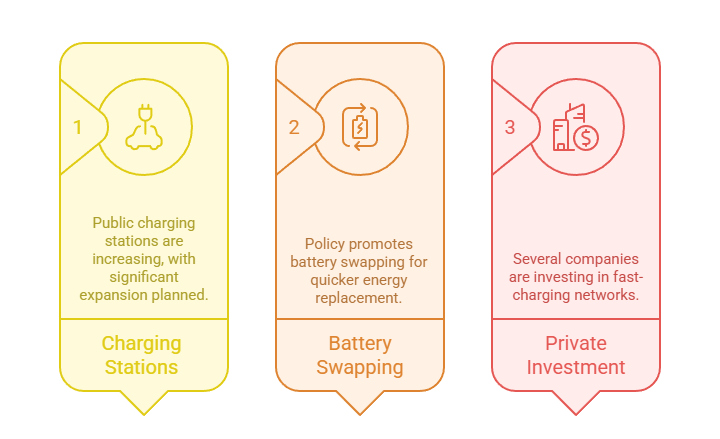

Public Charging Stations: Over 13,000 charging stations are operational (as of mid-2025), with plans to reach 100,000 by 2030.

Battery Swapping Policy: Drafted in 2022, this policy encourages interoperability for e-two and three-wheelers, enabling faster energy replenishment.

Private Sector Role: Companies like Tata Power, Statiq, Ather Grid, and Indian Oil are investing heavily in setting up fast-charging networks.

Challenges Hindering EV Adoption

Despite progress, several challenges remain:

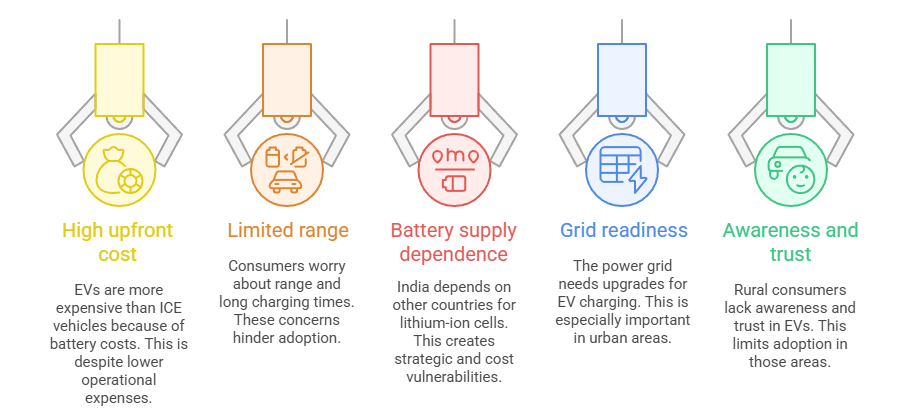

High upfront cost: EVs still cost 20–30% more than ICE vehicles due to battery costs, despite lower operational expenses.

Limited range and charging time: Consumer apprehensions about range anxiety and long charging durations persist.

Battery supply chain dependence: India relies heavily on China, South Korea, and Japan for lithium-ion cells, posing strategic and cost risks.

Grid readiness: The power grid must be upgraded to handle high EV charging loads, especially in cities.

Awareness and trust: Rural and semi-urban consumers lack adequate awareness and trust in EV reliability.

Recent Developments (2024–2025)

e-AMRIT 2.0: The government launched an updated version of its national e-mobility awareness portal to help consumers compare EV models, subsidies, and savings.

Green Urban Mobility Initiatives: MoHUA is supporting metro cities in deploying 10,000+ e-buses through VGF (Viability Gap Funding).

Global Partnerships: India joined the Global Battery Alliance and signed MoUs with countries like Australia and Argentina for lithium procurement.

Scrappage Policy Integration: The vehicle scrappage policy is being aligned with EV promotion to encourage end-of-life replacement with e-vehicles.

The Road Ahead: Future Outlook

India has ambitious EV targets:

By 2030:

70% of all commercial vehicles

30% of private cars

40% of buses

80% of two- and three-wheelers to be electric.

To meet these, a coordinated approach involving policy support, public-private partnerships, localization of battery production, and awareness campaigns is essential.

Conclusion

India’s electric vehicle revolution is well underway. With the right mix of innovation, incentives, and infrastructure, the country has the potential to become a global EV manufacturing and export hub. The shift to electric mobility not only promises cleaner air and reduced oil imports but also new economic opportunities, job creation, and a more sustainable future.

One comment