Relevance: Prelims/Mains: G.S paper III: Economy

Introduction:

- The Budget 2020-21, a reformative budget in the present economic scenario is the budget that cares for all the people of India across economic strata.

• The basic canon of this budget has been that in our journey towards development to make India a $5 trillion economy by 2024, no one is left behind.

• This budget woven around the themes of Aspirational India, the Caring India and Economic development for All is the guide map for the year 2020-21 to join hands together and advance on the path of economic growth together with the help of technology and innovations.

Key objectives:

- This is the Budget to boost people’s incomes, to provide more money in their hands, to enhance their purchasing power, to boost consumptions and therefore demand.

• The demand in turn would intensify growth cycle of the economy with jobs and gainful earnings.

• In this endeavour tax policy is critical as tax revenue is not only essential for undertaking expenditure to spur investment, employment and growth but is also essential for undertaking spending on priority sectors and welfare schemes which safeguards the welfare of the marginal sections of the population.

• Tax policy is also used to provide impetus to certain industries, regions and financial instruments by channelising savings and investment into specific areas based on the priorities of die Government with regards to economic policy and growth.

• With these objectives, the Budget 2020-21 focuses on fundamental structural reforms and inclusive growth.

• The Government’s aim is to make the tax department a department in dialogue with taxpayers which listens, trusts and believes you; which is using technology to provide convenience to genuine taxpayers and is judiciously equipped with data analytics and information triangulation to hit tax evaders and reduce leakages with targeted actions; which is faceless but friendly to serve taxpayers better; which is simple, online and helpful system with least possible legal disputes.

Budget highlights in respect of Indirect and Direct Taxes are:

- Indirect Taxes- GST Revised Estimate of CGST for current FY 2019-20 is Rs. 5,14,000 crore and the Budget Estimate of CGST for upcoming FY 2020-21 is Rs. 5,80,000 crore. A simplified return currently under pilot run shall be implemented from 1 April, 2020.

• It will make return filing simple with features like SMS-based filing for nil return, return pre-filling, improved input tax credit flow and overall simplification.

• Refund process has been simplified and has been made fully automated with no human interface.

• At the same time, data analytics and AI tools are being used for targeted crackdown on GST fake input tax credit, deceitful refund claims, and other frauds. Several measures have been taken for improving compliance.

• E-invoice will be implemented in a phased manner on optional basis to facilitate compliance and return filing. Aadhaar-based verification of taxpayers is being introduced. This will help in weeding out dummy or non-existent units.

• Dynamic QR-code is proposed for consumer invoices. GST parameters will be captured when payment for purchases is made through the QR-code. A system of cash reward is envisaged to incentivize customers to seek invoice/s. GST rate structure is also being deliberated so as to address issues like inverted duty structure.

Indirect Taxes- Customs:

- The Revised Estimate of Customs Duties for 2019-20 is Rs. 1,25,000 crore as against the Budget Estimate of Rs. 1,55,904 crore. Budget Estimate for 2020-21 is Rs. 1,38,000

crore. Besides several tax measures proposed in Customs in line with the stated policy direction of the government, suitable provisions for verification of beneficial duty claim arc being incorporated in the Customs Act to specifically provide for certain obligation on importer and prescribe for time bound verification from exporting country in case of doubt.

• In addition, changes are being made in certain provision of safeguard duty and the Anti-dumping Rules and Countervailing Duty Rules are being strengthened for the anti-

circumvention measures.

• To give boost to domestic industry, import duty on a number of products such as footwear, furniture, toys, tableware and kitchenware, stationery and other office items

and a number of domestic appliance and items of common use that are locally produced especially by the MSME sector, are being increased.

• A concerted effort has been made to increase domestic value addition in sectors like mobile phones and other electronics items, electric vehicles, battery, etc., through proper phasing of manufacturing activity.

• Customs exemptions have been reviewed to weed out entries that arc redundant, obsolete or outlived their utility and 80 such exemptions are being withdrawn by making suitable amendment/rescission of relevant notifications.

• A health cess is proposed, by way of custom duty, on the imports of medical equipment keeping in view that these goods are now being made significantly in India. The proceeds of this cess shall be used for creating infrastructure for health services in the identified districts.

Direct Taxes:

- Before we go on the direct tax proposals in the Budget 2020-21, let us have a look on the income tax scenario. The efforts undertaken by the income tax department arc reflected in the significant growth in overall tax collection, number of filers and taxpayers, etc.

• As a result of the efforts undertaken, the Indian economy has displayed high tax buoyancy with a buoyancy factor greater than 1, i.e., the rate of growth of direct taxes has been greater than the rate of growth of GDP.

• Apart from high tax buoyancy, between 2014-15 and 2018-19, the direct taxes have recorded a growth in collection of 64%.

• Further between FY 2013-14 to FY 2018-19 the number of return filers has grown by 91.02% while the number of taxpayers has increased by 60.55%.

• With this performance on income tax, the Budget emphasises on simplifying the direct tax administration and making the proposed Tax Charter the part of the statute. This is the yet another determined step to make the direct tax system taxpayer friendly in true sense.

• The Income Tax Act states taxpayers’ responsibilities. The Taxpayers’ Charter would state tax administration’s accountabilities towards taxpayers.

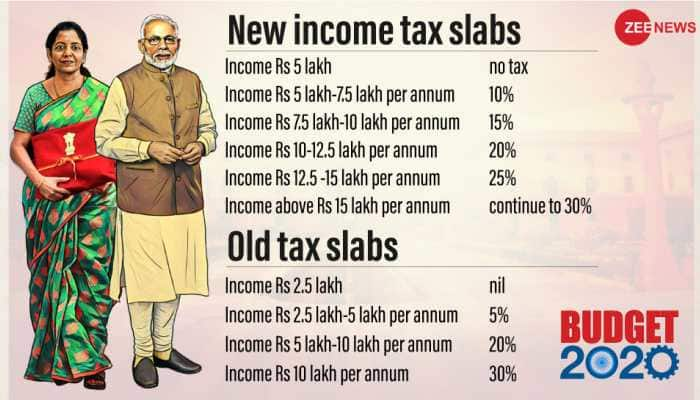

• In the budget, Dividend Distribution Tax (DDT) has been proposed to be abolished. The dividend now shall be taxed only in the hands of the recipients at their applicable tax slab rate. There have been several procedural easing alongside. It proposes to bring a new and simplified personal income tax regime where income tax rates will be significantly reduced for the individual taxpayers who forgo certain deductions and exemptions. Such relief is expected to give an impetus to the demand at estimated revenue forgone of Rs. 40,000 crore per year.

• The new tax regime shall be optional for the taxpayers hence an individual who is currently availing more deductions and exemptions under the Act may choose to avail them and continue to pay tax in the old regime.

• The Scheme gives complete waiver of interest and penalty if the Scheme is availed before 31 March, 2020.

• The objective of enhancing the efficiency of the delivery system of the Income Tax Department, the Budget proposes to provide that the CBDT shall adopt a Taxpayer’s Charter and issue necessary direction for the implementation of the same.

• To incentivize the investment by the Sovereign Wealth Fund of foreign governments in the priority sectors, the Budget proposes to grant 100% tax exemption to their income for investments made in India.

• In order to enable start-ups to attract talented employees by providing them Employee Stock Option Plan (ESOP). The Budget proposes to allow deferment of the tax payment by the employee for five years in respect of income relating to ESOP.

• To further incentivize the start-up ecosystem, the Budget also proposes to provide lax holiday to the large Start-ups having turnover up to Rs.100 crore and also to extend the period of availing the deduction from 7 years to 10 years. The Budget proposes to raise the turnover threshold for compulsory audit from the existing Rs. 1 crore to Rs. 5 crore.

• As it brings in an income tax regime that is not only hassle-free and less cumbersome but also lessens the burden of scrutiny and compliance on the taxpayers and minimizes the paperwork such as receipts maintenance, documentation and burden of proof.

For more such notes, Articles, News & Views Join our Telegram Channel.

Click the link below to see the details about the UPSC –Civils courses offered by Triumph IAS. https://triumphias.com/pages-all-courses.php