Introduction: India energy future

India energy future landscape is undergoing a pivotal transformation. Ensuring energy security—accessible, affordable, and reliable power—has become central to national growth and climate resilience. The strategy blends robust renewable capacity expansion, diversification of energy sources, strategic reserves, and modern infrastructure to reduce imports and enhance sustainability.energy crisis India

Current Energy Scenario: Supply, Demand, and Dependence

- Primary Energy Supply (PES) grew by 7.8% in FY 2023–24 to 9,03,158 KTOE, signaling post-pandemic recovery and rising energy needs.

- Coal still dominates, providing 79% of domestic energy supply and accounting for 60% of total primary energy supply (TPES).

- India imports over 89% of crude oil, 46.6% of natural gas, and 25.8% of coal, highlighting significant reliance on global markets.

Despite these trends, per‑capita electricity consumption remains low: about 1,106 kWh per person—well below the global average (~3,000 kWh), though rapidly rising.

Renewable Surge: Capacity vs Generation

- India achieved its Paris Agreement goal of having 50% non‑fossil installed power capacity in 2025—five years ahead. Out of 484.8 GW capacity, 242.8 GW comes from renewables and large hydro

- Installed renewable capacity grew from 81.6 GW in 2015 to nearly 198 GW in 2024, at a CAGR of 10.4%.

- India is now the world’s 3rd-largest solar power generator, surpassing Japan in 2023, with solar contributing significantly to global mix (India’s share ~5.9%).

Still, actual generation tells another story: in FY 2024, total electricity generated was 2,030 TWh, with renewables contributing only ~240 TWh, compared to 1,517 TWh from coal—renewables account for just ~24% of actual energy supply. Ind‑Ra expects renewables to remain at 21% of the energy mix in FY 2025, rising to 35–40% by.

Strategic Shifts: Policy Measures & Infrastructure

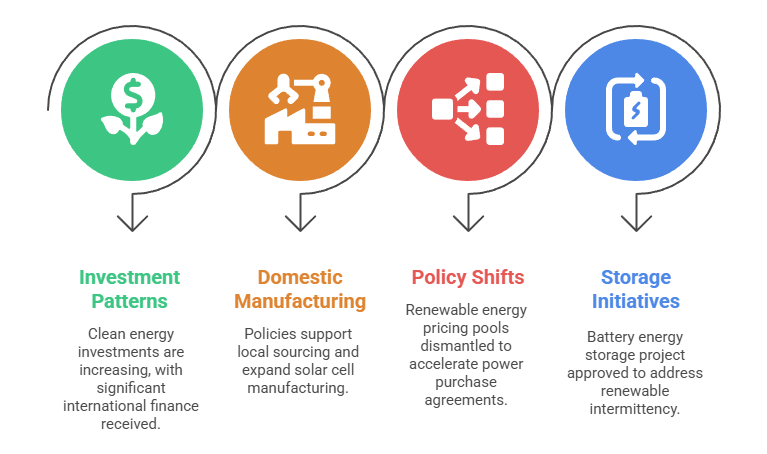

- Investment Patterns: In 2024, about 83% of power sector investment flowed into clean energy. India received USD 2.4 billion in international development finance and USD 5 billion in FDI for power generation and transmission.

- Domestic Manufacturing Push: Policies mandating local sourcing for wind turbines include blades, generators, and data localization requirements. These support domestic firms like Suzlon, Inox, and Adani Wind while limiting foreign imports.

Production-linked Incentives (PLI) and capital allocation schemes have expanded solar cell manufacturing capacity to ≈30 GW/year by March 2025, cutting China dependency.

- Tariff and Clean Energy Policy Shifts: India recently dismantled central renewable energy pricing pools to accelerate power purchase agreements and de-risk stranded projects. Over 50 GW of stranded renewable projects remain in limbo due to transmission/backlog issues.

- Energy Storage Initiatives: Kerala has approved a 125 MW / 500 MWh battery energy storage project, backed by ₹135 crore government support, to address renewable intermittency. It will provide four hours of daily stored energy at peak demand.

Coal’s Persistent Role and Transition Challenges

- Coal production rose to a record 1 billion tonnes in FY 2024–25, 70% of electricity still coal-generated. The Power Ministry plans an additional 90 GW coal-fired capacity by 2032, exceeding previous targets.

- Structural challenges hinder transition: financing constraints for utilities, grid integration issues, social dependency on coal-rich states, and underdeveloped storage. Without adequate infrastructure and retrofi.

Sectoral Highlights & Local Inclusion

- India added 21 GW solar and 3 GW wind capacity in 2024, bringing total utility renewables to over 220 GW

- The Bhadla Solar Park in Rajasthan—India’s largest at 2.245 GW—helps reduce emissions by ~4 million tonnes/year and supports rural employment (~10,000 jobs)

- As of June 2025, installed capacity stands at 484.8 GW, of which 46.3% is non-fossil (including 116 GW solar, ~52 GW wind, 10.7 GW biomass, 5.1 GW small hydro, and 8.2 GW nuclear).

Key Policy Imperatives for Energy Security

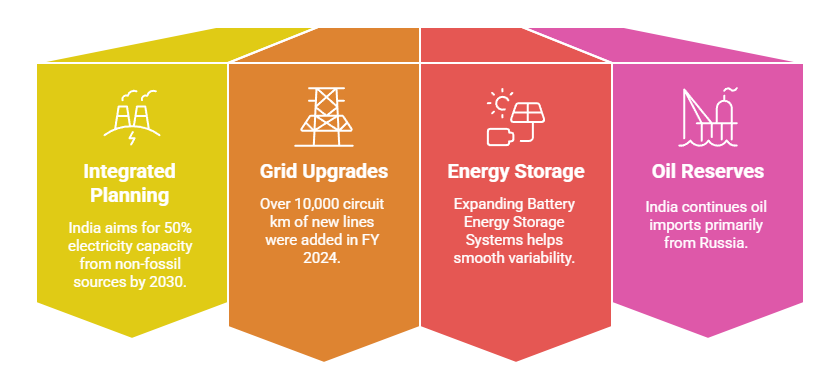

- Integrated Planning: India aims for 50% electricity capacity from non-fossil sources by 2030, with 100 GW solar, 60 GW wind, and 100 GW nuclear by 2047. Completion requires legislative support and private-sector participation reforms in nuclear energy.

- Grid and Transmission Upgrades: Over 10,000 circuit km of new lines and 71,000 MVA transformation capacity were added in FY 2024. Conductive grid infrastructure is critical to absorb intermittent renewables and reduce T&D losses (which fell from 23% to 17%) .

- Energy Storage and Hybrid PPA Tenders: Expanding Battery Energy Storage Systems (BESS) and hybrid solar-wind tenders helps smooth variability. Policies now support hybrid projects and round-the-clock power flowering.

- Strategic Oil Reserves and Supply Diversity: India continues oil imports primarily from Russia (~36–40% in early 2025) despite U.S. threats of tariffs. Government emphasizes energy sovereignty, while exploring alternatives to buffer price shocks and geoeconomic risks

Challenges Ahead & Strategic Recommendations

- Low per capita usage: Despite progress, electricity consumption per person (~1,395 kWh in 2023‑24) still trails global peers, highlighting large unmet energy needs.

- Stranded assets: Without timely PPA and transmission, more than 25% of installed capacity is stranded, delaying India’s energy targets and threatening project viability.

- Financing and affordability: State utilities remain stressed; aggressive tariffs and delayed:

compliance hamper renewables. Lower financial costs and reform in distribution is needed.

- Coal dependency: With employment and regional reliance tied to coal, a just transition strategy—upskilling, alternate livelihoods—is essential.

Conclusion

India’s energy security strategy hinges on an ambitious yet fragile balancing act—rapidly scaling renewables while managing coal dependence, diversifying energy geography, securing critical infrastructure, and investing in sustainable grids and storage. Achieving a future energy system that is resilient, low-carbon, and accessible will demand continued policy innovation and execution discipline. |

2 comments