Introduction

Microfinance, as a financial mechanism targeting low-income households, is not just an economic instrument but a tool of social transformation. In India, it serves as a bridge between marginalized communities and formal financial institutions, addressing structural inequalities and fostering economic empowerment. Sociologically, microfinance can be seen as an intervention aimed at reducing poverty, enhancing agency, and promoting social cohesion. Thinkers such as Amartya Sen and Pierre Bourdieu provide critical insights into the societal implications of financial inclusion, highlighting its potential for enhancing human capabilities and reshaping social capital. Les us explore the dynamics of microfinance in India, its challenges, policy interventions, and the broader sociological implications for social inclusion, gender empowerment, and equitable development.

Microfinance and Its Role in Social Inclusion

Microfinance institutions (MFIs)—including NBFC-MFIs, small finance banks, and commercial banks—serve nearly eight crore poor households by providing doorstep, collateral-free loans, savings facilities, and financial literacy programs. From a sociological perspective:

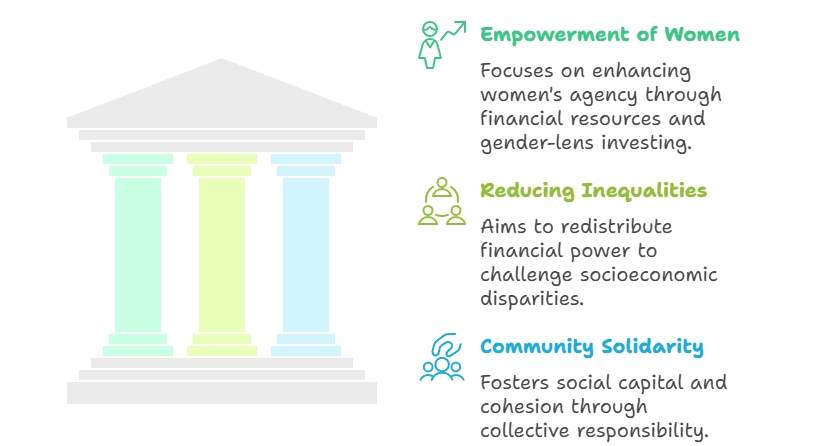

- Empowerment of Women: Drawing on Amartya Sen’s capability approach, microfinance enhances women’s agency by giving them access to financial resources. Gender-lens investing prioritizes women entrepreneurs, recognizing the multiplier effect on household well-being and community development. Studies have shown that female borrowers are more likely to invest in children’s education and healthcare, reflecting broader social benefits.

- Reducing Socioeconomic Inequalities: According to Karl Marxian theory, economic disparities underpin structural inequalities. Microfinance attempts to redistribute financial power by enabling marginalized groups to access credit, thereby challenging entrenched class hierarchies.

- Community Solidarity and Social Capital: Borrowing from Pierre Bourdieu, MFIs foster social capital through joint liability groups, peer monitoring, and collective responsibility. These mechanisms enhance trust and social cohesion within communities, echoing Durkheim’s functionalist perspective, where solidarity is critical to societal stability.

Trends Shaping Microfinance Funding

The microfinance sector in India has evolved in response to technological, financial, and social trends:

- Digital Transformation: Fintech collaborations reduce operational costs and improve credit assessment. Digital lending platforms facilitate financial inclusion in remote regions, enabling more efficient access to credit.

- Blended Finance Models: By combining concessional funding with commercial capital, MFIs can de-risk investments, attract private sector participation, and expand outreach.

- Green Microfinance: Environmentally sustainable projects, such as solar energy loans or climate-resilient agriculture, are increasingly prioritized, linking microfinance to ecological development goals.

- Gender-Lens Investing: Investors are focusing on MFIs that empower women, consistent with sociological findings that women’s economic participation strengthens familial and community structures.

Challenges Facing Microfinance in India

Despite its promise, the microfinance sector faces multiple challenges that threaten its social and economic objectives:

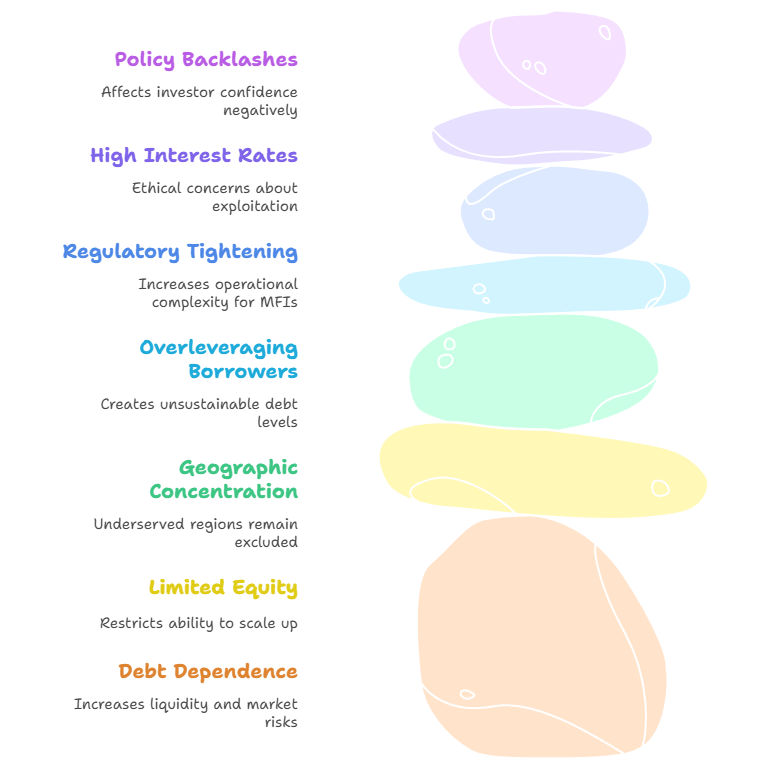

- Overdependence on Debt Capital: Most MFIs rely heavily on loans from banks and financial institutions. During economic downturns or interest rate fluctuations, this exposes them to liquidity risks, undermining their capacity to serve marginalized communities.

- Limited Equity Infusion: Investor caution regarding asset quality, regulatory risks, and limited exit options restricts MFIs’ ability to scale, curbing their social impact.

- Geographic Concentration: Microfinance lending is heavily concentrated in approximately 250 districts, leaving the Northeast, tribal belts, and other underserved regions largely excluded. This challenges the sector’s mission of equitable inclusion.

- Overleveraging of Borrowers: Multiple loans from different institutions have led to unsustainable debt levels. In states like Odisha, Kerala, Tamil Nadu, and Rajasthan, average loan outstanding per borrower often exceeds per capita income, risking repayment defaults and financial distress.

- Regulatory Tightening: RBI’s regulations, including stricter income assessments and repayment caps (50% of household income), protect borrowers but increase operational complexity and slow loan disbursals.

- High Interest Rates and Shrinking Portfolios: Despite access to low-cost capital, MFIs charge high margins to cover risks, raising ethical concerns about borrower exploitation. The gross loan portfolio fell by 13.5% to ₹3.75 lakh crore in FY25 due to cautious lending.

- Historical Policy Backlashes: Events like the Andhra Pradesh microfinance crisis of 2010 still affect investor confidence and sectoral reputation, despite the Supreme Court overturning restrictions in 2023.

Government Initiatives and Regulatory Framework

The Indian government and RBI have introduced multiple measures to strengthen the sector and ensure sustainable growth:

- RBI Unified Regulatory Framework (2022):

- Standardizes microfinance loan definitions, repayment schedules, and income assessments.

- Caps repayment at 50% of household income to prevent over-indebtedness.

- Requires reporting of household income to Credit Information Companies (CICs), enhancing transparency.

- PM SVANidhi Scheme:

- Provides working capital loans to street vendors with enhanced loan limits and digital payment incentives.

- Expanded to include census towns and peri-urban areas, fostering broader financial inclusion.

- RBI Advisory Role in MSME Credit Flow:

- Promotes digital credit assessment tools, unified lending interfaces, and fair lending practices.

- Encourages proactive rehabilitation for distressed borrowers, balancing financial sustainability with social responsibility.

Sociological Implications of Microfinance

- Social Mobility and Poverty Reduction: Microfinance provides opportunities for upward mobility by enabling marginalized groups to invest in income-generating activities. This aligns with functionalists’ view that institutions contribute to social stability and opportunity.

- Changing Household Power Dynamics: With women gaining access to financial resources, traditional patriarchal hierarchies are challenged, reflecting Feminist Sociological Theory. Women’s decision-making power within households increases, influencing resource allocation and child welfare.

- Community Transformation: Group lending models promote collective responsibility, reducing social isolation and fostering community networks. Bourdieu’s concept of social capital explains how trust, norms, and networks created through MFIs strengthen collective resilience.

- Potential Risks and Ethical Concerns: Overleveraging and high interest rates may lead to social distress, highlighting Marxian critiques of exploitative capitalist structures even within socially oriented initiatives.

Path to Sustainable Growth

For microfinance to realize its sociological and economic potential, several strategies are critical:

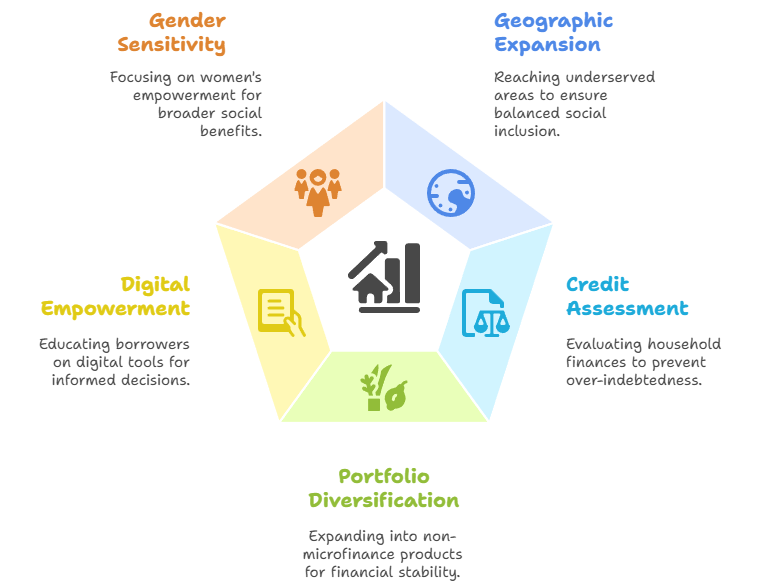

- Geographic Expansion: Targeting underserved areas ensures that social inclusion is balanced across regions.

- Strengthening Credit Assessment: Accurate evaluation of household income and liabilities prevents over-indebtedness.

- Diversification of Portfolios: MFIs should cautiously expand into non-microfinance products to ensure financial stability without compromising social objectives.

- Digital Empowerment and Financial Literacy: Educating borrowers and promoting digital financial tools enhance informed decision-making and responsible borrowing.

- Gender-Sensitive Programs: Continued focus on women’s empowerment amplifies social and economic benefits at household and community levels.

Conclusion

Microfinance in India operates at the intersection of economic policy and social change. While it offers a pathway for inclusion, empowerment, and poverty alleviation, the sector faces significant challenges that must be addressed through regulatory prudence, innovative financing, and technological integration. From a sociological perspective, MFIs are not merely financial intermediaries—they are agents of social transformation, shaping household dynamics, community solidarity, and gender relations. Thinkers like Amartya Sen, Pierre Bourdieu, Karl Marx, and feminist sociologists provide valuable frameworks to understand the implications of microfinance beyond economics. For sustainable growth, microfinance must harmonize financial viability with its social mission, ensuring that access to credit translates into genuine empowerment and equitable development across India.

|

One comment