India’s Path to a Manufacturing Renaissance

(Relevant for GS paper-3, Economic Growth)

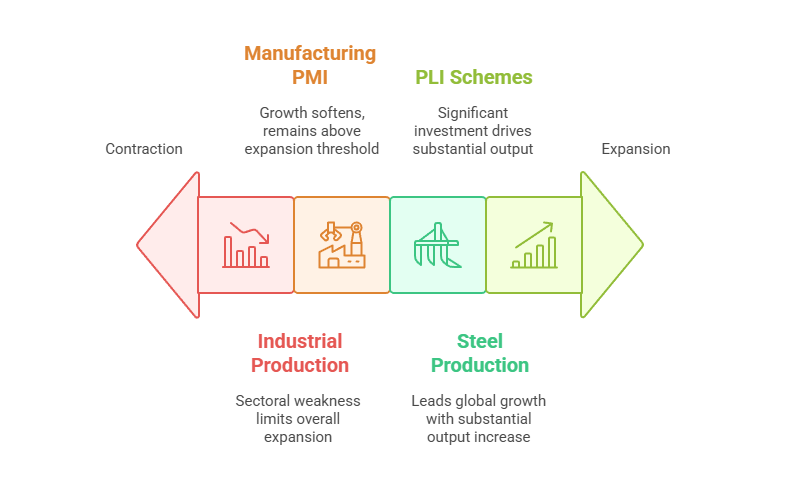

Path to a Manufacturing RenaissanceIndia stands at a defining moment in its economic journey. With the manufacturing sector’s GDP share hovering around 17–17.7%, the nation remains short of targets set for 25% by 2025 under the National Manufacturing Policy and Make in India initiatives UPSC aspirants, understanding the opportunities and challenges in re-shaping this landscape is crucial. Recent Performance & Sector Outlook

National Aspirations & Policy MomentumMake in India & PLILaunched in September 2014, Make in India aimed to raise manufacturing’s share to 25%. That target remains unmet; the share fell from 16.7% (2013–14) to ~15.9% (2023–24). Nonetheless:

Infrastructure & Logistics – PM Gati Shakti, NIPThe PM Gati Shakti national master plan integrates seven infrastructure “engines” (rail, road, port, waterway, airport, mass transport, logistics), promoting multi-modal logistics Complementing this:

Atmanirbhar Bharat & Sector Initiatives

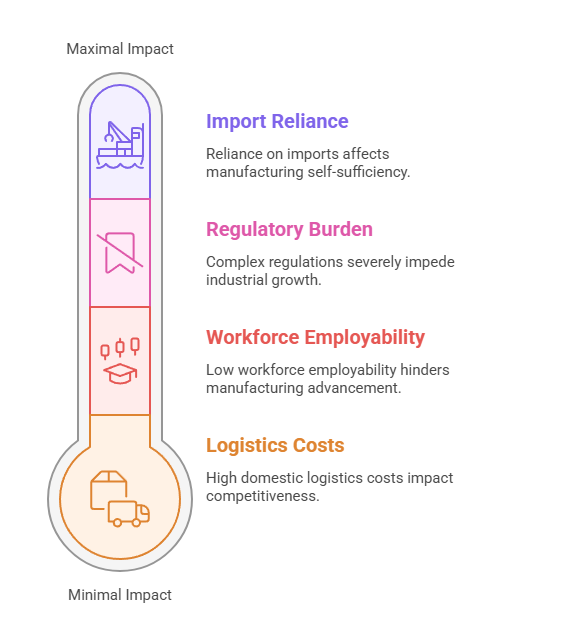

Remaining Challenges

Despite these policy lights, critical obstacles remain:

Domestic logistics remain costlier than global peers (14–18% vs 8–10% GDP), with India ranking only ~38th in the World Bank Logistics Performance Index. Infrastructure gaps and bottlenecks persist despite Gati Shakti initiatives.

Only 24–49% of the workforce is employable for modern manufacturing jobs, far behind developed economies R&D spend hovers around 0.7–1% of GDP, marginal compared to South Korea’s and China’s levels (~2–4%)

Complex labor law and land acquisition procedures still hamper growth; contract enforcement lags (India ranked 163rd in the World Bank’s Doing Business in 2020) . Bureaucratic delays continue affecting large industrial plans.

India remains reliant on imports for semiconductors, electronics, natural gas, specialized machinery and raw materials. The trade deficit with China was ~$85 billion in FY23‑24 Steel production exceeds domestic ore output, forcing imports to ramp up by 2030 Strategic Imperatives for a Manufacturing Surge

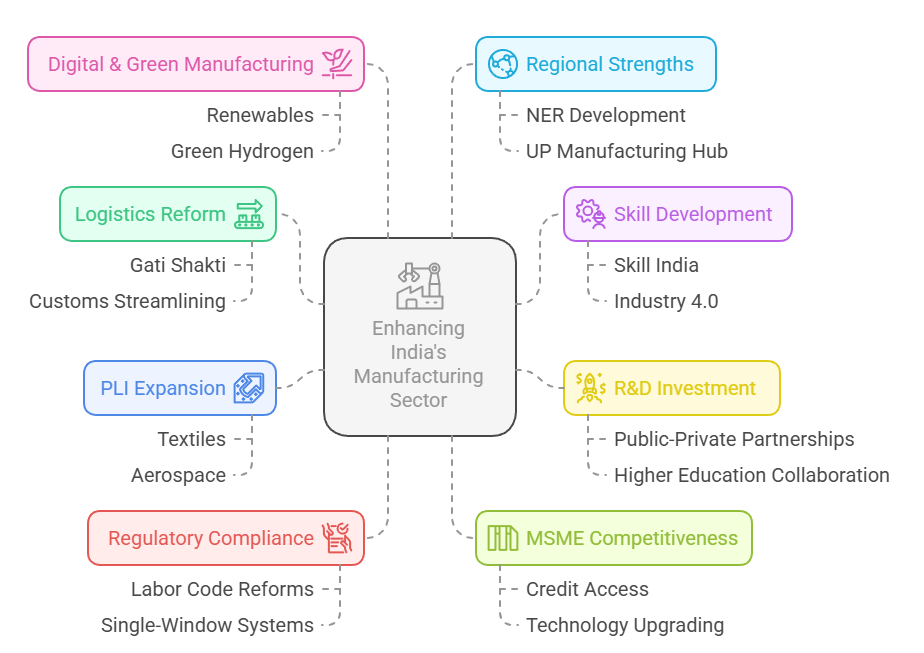

To unlock potential toward targets of 25% by 2047 and 15% annual sector growth per NITI Aayog, India must:

Global Positioning & UPSC RelevanceIndia’s transition from being just the world’s fourth-largest auto producer to becoming the second-largest smartphone manufacturer, powered by Apple, Samsung, and PLI-driven investments, underlines an emerging China + 1 alternative positioning The automotive sector employs millions and contributes over 7% to GDP; India ranks as the 3rd largest car market in 2025 Manufacturing’s future alignment with global value chains and resilience to geopolitical shocks will also influence macroeconomic indicators, employment generation, federal budget sustainability, and economic diplomacy—all key themes in the UPSC GS Paper‑III. ConclusionIndia’s manufacturing sector is at a pivotal juncture. Strong policy frameworks—from PLI to Gati Shakti—have laid a sturdy foundation. Yet, to meet the ambitious targets of 25% GDP share, 15% annual growth, and emerge as a global supply chain hub, India must overcome systemic friction in infrastructure, skills, technology, regulatory ease, and supply‑chain resilience. With strategic implementation and course correction, the next two decades could witness a renaissance in Indian manufacturing—fulfilling its potential as an engine of growth, employment, innovation, and sustainable development. For UPSC aspirants, articulating these linkages and policy proposals coherently can demonstrate a nuanced understanding of one of India’s most crucial economic frontiers. |

To Read more topics, visit: www.triumphias.com/blogs

Read more Blogs:

Solutions to the Problem of Farmers Distress & Suicide | Triumph IAS

2 comments