Covid-19 Relief Package for MSMEs Analysis

Relevance: Mains: G.S paper III: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment. • Inclusive growth and issues arising from it.

• Government Budgeting.

CONTEXT

The Covid-19 relief package for micro, small and medium enterprises and the changes to the defining criteria for MSMEs are examined. While the changes in the MSME definition open the sector to larger enterprises, the composite criteria introduce fresh ambiguities to the defining of MSMEs. Liquidity infusion measures at this juncture without adequate measures to revive demand will not help MSMEs tide over the Covid-19 lockdown-induced crisis.

ANALYSIS

The micro, small and medium enterprises (MSMEs) are of immense importance to the Indian economy, in terms of generating employment, output, and exports.

Yet, it is a sector that is vulnerable, and can quickly become unstable and unviable, particularly in the presence of external shocks. In recognition of these aspects, the finance minister announced the much-awaited relief package for the MSMEs on 13 May 2020 to tide over the Covid-19 lockdown-induced crisis.

The announcements also included a change in the defining criterion for MSMEs. I discuss what the change means for the sector. The gaps in the response of the state to ensure viability of the MSME sector in the midst of the ongoing pandemic are explored and some specific recommendations are offered.

Defining MSMEs

Any priority sector scheme that seeks to target beneficiaries, includes certain entities and excludes others. Thus, defining these entities becomes important. Being classified as MSMEs provides enterprises some handholding by the state, making them eligible for certain benefits. These include priority lending from banks, collateral free loans, mandatory sourcing of 25% of procurements by the central government from micro and small enterprises (MSEs), and a slew of other targeted benefits.

Identifying what qualifies as a small and medium enterprise (SME) has been a contentious issue for decades. Internationally, consensus on a uniform norm has been hard to achieve (Berisha and Pula 2015), and the most accepted ones are from the World Bank and the International Finance Corporation based on the criteria of employment, assets, and turnover, where a unit has to fulfil the employment criteria, and any one of the two financial criteria to qualify as an SME.

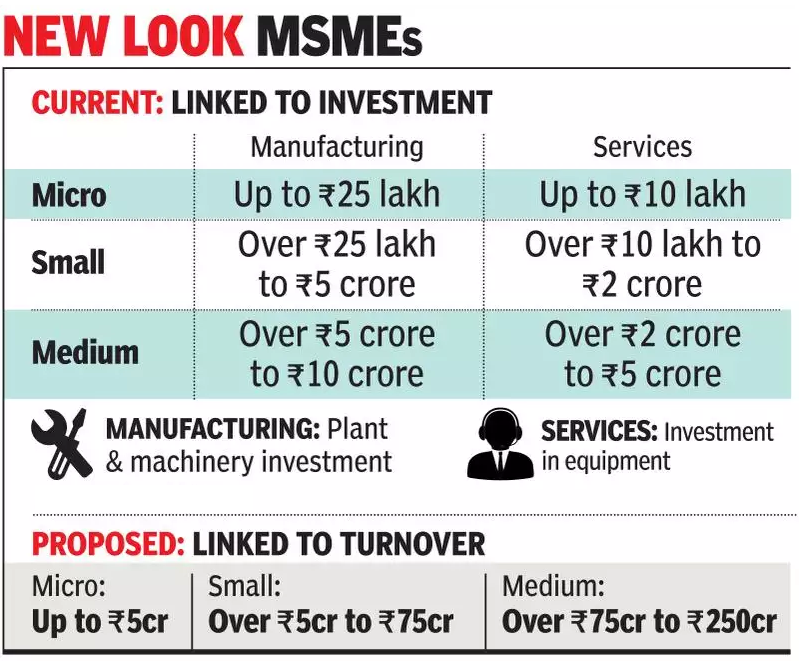

In India, MSMEs were defined by the MSME Development Act of 2006 for the first time. The act used investment in plant and equipment for manufacturing and in equipment for services (excluding investments in land and building, costs of research and development and pollution control devices, etc) as the defining criteria.

The recent changes in the definition of MSMEs follow a composite criterion, using both turnover and investment in plant and machinery. They also eliminate the difference in investment thresholds between the manufacturing and services sector.

While threshold revisions to adjust for inflation itself are a routine task, there has been deliberation in the past with the MSME Development (Amendment) Bill 2018 introduced in the Lok Sabha to define MSMEs by the turnover criteria alone.

With the Goods and Services Tax (GST) Act in place, a measure of turnover was seen as an easier and a more transparent way to define MSMEs. This was, however, met with stiff resistance on the grounds that the turnover thresholds were too high, and defining the MSMEs by turnover alone would expand the group to include much larger units (Sinha 2018).

Investment size and turnover criterion: Defining MSMEs by the investment criteria has one major weakness: the “original” investment in plant and machinery or equipment criteria does not offer a level playing field to newer entrants in the market.

An older plant would show substantially depreciated investments in its book of accounts. This unit would qualify as a much smaller unit, while any new entrant that needs similar machines would have to make much higher investments.

Thus, what would be a micro unit because of historical book value of investments, would be classified as a much larger unit if set up many years later. In this sense, the annual turnover-based criteria to define the sector might be much more meaningful. Also, calculating reinstated costs of machinery is a cumbersome and costly process, and entails physical verification, often requiring the assistance of a chartered accountant, and hence, additional transaction costs. Turnover can be far more transparent, particularly now that a large number of MSMEs are under the ambit of the GST.

The turnover criterion was criticised as it might provide an incentive to under-report and qualify as an MSME. Though, under-reporting investment size is also a possible route for a unit to remain classified as an MSME. So, a solution to under-reporting per se cannot be addressed through changes in the criteria for defining the MSMEs. Instead, that would require monitoring and inspection.

The new composite criterion has come in with lower turnover thresholds than what the 2018 amendment bill had proposed. However, it does not undo the problems that stem out of using the original size of investment in plant and machinery as a criterion.

Importantly, the composite definition has assumed a turnover of five times the investment for the three categories of enterprises. Such an assumption does not consider the varied nature of the MSMEs.

For certain sectors, the gems and jewellery sector, for example, a huge turnover is achieved due to the very nature of the final product, even with a much smaller investment in plant and machinery.

Similarly, a leather unit, which is a highly labour-intensive sector, can achieve a much higher turnover with low capital investments. On the other hand, there are sectors that have higher capital investments but lower turnovers. These aspects would be of importance to certain industrial sectors and would require attention so that the sectors that are particularly important to employment generation do not fall out of the MSME ambit.

The employment criteria: The Annual Report 2018–19 released by the Ministry of MSMEs estimates that there are around 634 lakh unincorporated non-agricultural MSMEs based on the 73rd National Sample Survey (NSS) in 2015–16. About 31% units are in manufacturing, 36.3% in trade, 32.6% in other services, and a minuscule proportion in non-captive electricity generation and transmission. These provided a total employment of 11.1 crore in 2015–16 (with 32.5%, 34.8%, 32.6% and 0.01% in the four categories respectively).

These are the “unorganised sector” enterprises alone, and excludes those MSMEs that would be registered under (i) Sections 2(m)(i) and 2(m)(ii) of the Factories Act, 1948; (ii) Companies Act, 1956 [together understood as the “organised manufacturing sector” where data is collected through the Annual Survey of Industries]; and (iii) the construction activities falling under Section F of National Industrial Classification (NIC) 2008.

The fourth census of MSMEs, though dated, could provide a sense of proportion of the MSMEs in the organised (or registered) and the unorganised (or unregistered) sector, showing that the bulk of the MSMEs (more than 94%) would be in the unorganised sector.

The organised and the unorganised sectors in India, however, are understood by an employment-based criterion, where registration under the Factories Act, 1948 (“the organised sector”) would mean an employment of 10 workers or more if working with electricity and 20 workers or more if working without electricity.

Thus, it should have been easy to define the MSMEs in India, too, as per the international norms, by the employment criterion. The stated reason for not applying this criterion to define MSMEs in India is the shifty nature of employment that the MSMEs generate, and the flexibility it has, to take care of its business cycles through non-permanent, causal, contractual, and/or daily piece-rate workers. The employment criterion is seen as a problematic measure to define MSMEs in India, due to the difficulties in counting this nature of non-permanent, highly flexible labour.

Neglect of Micro Enterprises

The NSS 73rd round found that 99.5% of these unorganised units are in the micro category of enterprises as per the erstwhile definition of MSMEs. The micro sector with 630.52 lakh estimated enterprises provides employment to 1,076.19 lakh persons, which accounts for around 97% of total employment in the unorganised sector

It is thus important to gauge the needs and policy directions for the micro sector separately from the much larger SMEs. Except for lip service, so far, not much attention has been paid exclusively to the micro sector’s viability, working capital requirements, credit leveraging capacities, or its market access.

The new composite criterion expands the micro category to an investment size of `1 crore (from the erstwhile `25 lakh) and a turnover of `5 crore. This essentially means that a number of units, which are much larger will now be clubbed together under the micro category itself. The possibility of a focused attention to this sector will be further diluted, both in terms of understanding the sector’s requirements, as well as the data collected.

This enlargement of the universe of the MSMEs is being implemented at a time when the global economy is at a standstill due to a pandemic that has left the Indian economy, and particularly the MSMEs, with an extremely uncertain future. While the government has claimed that the definitional changes respond to the fear of the MSMEs outgrowing the investment thresholds and thus losing benefits, the increased limits at this juncture only allow the bigger units to come under the MSMEs ambit to avail benefits.

COVID-19 and State Response

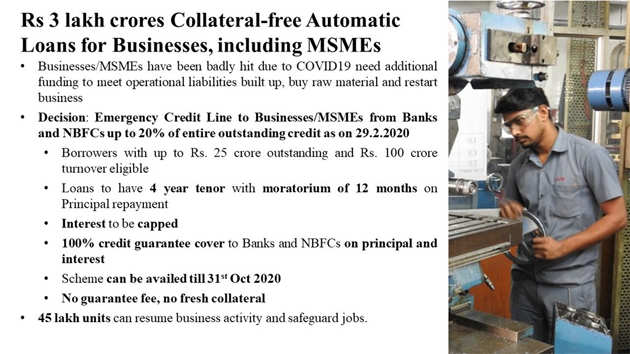

The central government, in recognition of the near complete disruption of economic activities of the MSMEs, has approved a set of measures to help the sector. These are in the form of collateral free automatic loans to the tune of `3 lakh crore over the next five months, fully guaranteed by the government; subordinate debt for stressed MSMEs and partial credit guarantee schemes; and funds to provide equity for MSMEs for stock exchange listing. While there is global recognition that this economic recession needs a demand-side fix, the government has essentially decided to infuse liquidity, a supply-side solution.

Limited number of beneficiaries: A small number of firms can actually reap the benefits from these schemes. The only firms eligible for collateral free loans at concessional rates are those that already have an outstanding loan. These 45 lakh firms, that is, only around 7% of the total estimated MSMEs, could borrow 20% of their outstanding credit as on February 2020.

While allocated funds for equity could be a measure to help medium-sized enterprises in normal times, in an emergency such as the present, these do not make much sense. Also, as mentioned before, the enlargement of the definition of MSMEs further marginalises the smaller enterprises and allows larger firms to come into the ambit of medium enterprises.

Similarly, while the announced `20,000 crore of subordinated debt for stressed MSMEs would provide some relief and be much appreciated in normal circumstances, there is the possibility of a greater number of firms accumulating stressed assets (non-performing assets) due to inadequate demand.

Effective demand: Firms that are in dire need of a fix to their demand problem4 are asked to borrow more, albeit on easier terms, to tide over the crisis. However, without adequate orders, firms would not be willing to borrow more (Purohit 2020). The finance minister has also acknowledged that firms were urging banks to not disburse sanctioned loans. Clearly, when millions of people have lost employment and purchasing power in the midst of a pandemic, firms would not want to produce more goods without effective demand. They are well aware that supply does not create its own demand, and hence would not be willing to borrow more. This causes a vicious circle, where lower production leads to a further reduction of employment opportunities and a further compression of demand.

Closing the Gaps

An important announcement that could actually help the MSMEs right away is the repayment of dues owed to them by the central government and the private sector that are to the tune of `5 lakh crore (Magazine and Sasi 2020). Instead of loans, the MSMEs that suffer from a dearth of working capital as well as delayed payments would be benefited if their dues are paid promptly. On 13 May 2020, the government promised to pay the MSMEs their dues within a span of 45 days. Along with this, the GST refunds need to be expedited. These measures would make the units atmanirbhar (self-dependent).

A public provision for at least a partial wage guarantee for MSME workers for the period of lockdown and for three months after the lockdown could help the employers and generate incomes.

Without adequate orders, units will produce less and employ fewer people, making some form of government-backed wage guarantee important in this situation.

The Supreme Court has already ordered that the units that do not pay full wages to their workers during the lockdown cannot be prosecuted (Rautray 2020). To be going out of business (particularly for small businesses) and being prosecuted hardly seems fair.

Also, a huge majority of MSMEs employ contractual, piece-rate paid labour. It would not be difficult for the employers to decline wages as workers would not have adequate papers to show an association with the enterprise. A wage guarantee programme becomes important in this context.

A bailout from paying electricity charges at least partially for a certain period of time would greatly help the MSMEs. Only infusing liquidity would not help small businesses and could lead to a further deterioration of the twin balance sheet crisis that is sure to emerge if demand does not revive.

For more such notes, Articles, News & Views Join our Telegram Channel.

Click the link below to see the details about the UPSC –Civils courses offered by Triumph IAS. https://triumphias.com/pages-all-courses.php